Buying a property is a hugely important and exciting moment in anyone’s life. It is a time to look ahead to a bright and promising future. At Prime Invest, we appreciate that the average person might find the whole process of buying a property a long and drawn out affair. That’s why we want to help you to understand the various stages involved, and the steps you need to take from the moment the last brick is laid until you finally take delivery of your new home. A number of formal procedures must be completed during this period.

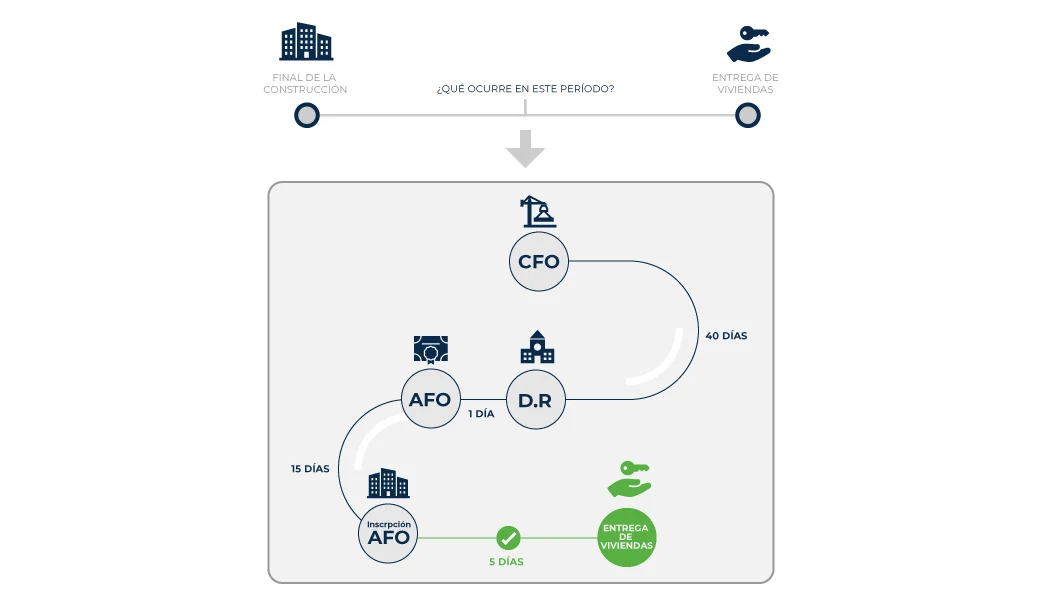

Firstly, once the work is completed, the Project Management Department of the construction company issues the Certificate of Completion of Building Work (in Spanish, CFO) and hands this over to the developer. This document must also receive official approval from the Architects Association. With this certificate in hand, the developer goes to the local council and submits the Declaration of Responsibility.

In terms of paperwork and time, the Declaration of Responsibility has simplified the process of applying for the First Occupancy Licence (in Spanish LPO). The Declaration of Responsibility submitted to the corresponding local council is a written statement providing evidence that the interested party has personally committed to carry out a series of procedures and to comply with all the requirements established by law. This Declaration has the same validity as the First Occupancy Licence when it comes to executing the deeds of sale or declarations of new construction required for subsequent registration of the property in the Land Registry.

Having completed these formalities, the developer brings together all the necessary documents and submits them to the Notary. At this point, the "Record of Completion of Building Work (in Spanish, AFO)" is signed, which certifies that the work and construction have been carried out and completed in accordance with the approved project and the previously granted licences. This record is entered in the Land Registry, and from this moment, the home in question is no longer listed as "work in progress" but as "completed work". Having submitted this certificate, it normally takes 3 weeks for the property to be officially entered in the Land Registry and recorded in the search note for the land on which your home is located.

Work can then begin on the execution of deeds and the handover of the property, and your private contract can be converted into a public deed of sale in order to complete the legal transaction of the sale.

Now that you have a general idea of the procedures that must be carried out before the delivery of a home takes place, let’s look at the steps that you, as buyer, must follow.

Imagine that you arrive at a completed residential development, you see the house of your dreams, and you decide to buy. When buying off-plan, the procedure begins with the signing of the reservation contract, which reserves the property in your name, continues with the signing of the private sales agreement, and concludes with the signing of the Deed in the presence of a Notary.

When the work is completed, it is standard practice to dispense with the private contract, and to simply sign a reservation, pay a small deposit and sign the deed within 30 to 90 days. If the buyer is a non-Spanish national, it is essential to provide a Foreigner’s Identity Number (NIE) and a Spanish bank account.

Prior to the official completion of the sale in the presence of the Notary, the buyer must successfully undergo a Prevention of Money Laundering (PBC) audit, which is designed to check that the buyer has obtained the funds for the purchase of the property in a legitimate manner. This can be demonstrated, for example, by providing your three most recent payslips, your tax declaration, the deed of sale of another property, etc. The buyer must receive approval by the Prevention of Money Laundering Audit before going to the Notary’s office.

If you have not yet seen your completed property, you can make a courtesy visit while this process is under way. This courtesy visit is not to be confused with the visit following the signing, which is when the checklist is drawn up.

Once the Prevention of Money Laundering Audit has received approval, and the documentation is in order, and the courtesy visit has been carried out, the big moment arrives: the Official Execution of the Sale in the presence of a Notary.

Before starting on the whole process, you will have had to fill in a form, often referred to as Know Your Costumer (KYC), in which you indicate whether you are financing the purchase with your own funds or with a mortgage. Let’s look at both cases:

- Own funds.

At the risk of stating the obvious, if you buy a property with your own funds, you do not need to contact a bank. You only need to be able to provide the necessary financial documentation that proves that the funds have been obtained in a legitimate manner.

Remember that there is a period of 3 weeks between the moment the developer submits the Record of Completion of Building Work and the time when the property is officially entered and published in the Land Registry. If the buyer so wishes, it is common practice to execute the deed in the presence of a Notary within this 3 week period.

- Subrogation or mortgage financing with third parties.

If you opt for financing, there are two options:

- Subrogation of the developer’s loan. The buyer has the option of substituting themselves for the seller and becoming the new holder of the loan requested by the developer for the construction of the property. The conditions for this type of financing are usually more advantageous for the buyer. It should be borne in mind that, by opting for this type of financing, your mortgage will be with the bank that has financed the developer, which will save on costs like the appraisal fee.

- Mortgage loan with other financial institutions: The other option is to apply for a new mortgage with the financial institution of your choice.

Once you have decided which financial institution is going to manage your mortgage, it is time to move on to the processing of your mortgage.

You will need to submit documentation relating to your personal, employment and tax situation, which are essential in order to carry out the corresponding feasibility study and risk assessment. As a general rule, a bank usually takes between 15 and 45 days to give you an answer.

Once the mortgage has been approved, we move on to the appraisal, registry verification and final approval. But before entering into the mortgage, current law is designed to ensure that the interested parties fully understand what they are about to sign. The following documents and services are included in this process:

- The European Standardised Information Sheet (ESIS) and the Standardised Warnings Sheet (SWS).

- The draft contract, with all costs itemised.

- Complete information on the costs of the transaction, and to whom they correspond.

- A written copy of the conditions and guarantees of any insurance policies taken out.

- A signed statement from the borrower. This signature confirms that you have received all the above information and that it has been fully explained to you.

- Mandatory and free advisory service before a notary chosen by the borrower. This final consultation in the presence of a notary confirms that you have fully understood the contracts, products, interest, allowances and other obligations and rights that apply to you as buyer

You are now ready to sign the deed of sale and mortgage, and become the owner of your new home!

Share this: